Karnataka 2nd PUC Accountancy Answer Key 2026 LIVE: Unofficial Key by Subject Expert; Difficulty Level Analysis

Karnataka 2nd PUC Accountancy Answer Key 2026 LIVE: Unofficial Key by Subject Expert; Difficulty Level AnalysisKarnataka 2nd PUC Accountancy Exam 2026 LIVE: Karnataka 2nd PUC Accountancy exam was successfully conducted on March 14, 2026, from 10 AM to 1 PM . Candidates can check the Karnataka 2nd PUC Accountancy answer key 2026 here, along with the paper analysis. There were 1 mark MCQs, 2 marks short questions, 6 marks, and 12 marks long answers. Some of the most important chapters that were asked in the exam were Retirement & Death of a Partner, Dissolution of Partnership Firm, and Accounting for Share Capital. Candidates will get approximately 16 marks from each of these units.

Karnataka 2nd PUC Accountancy Answer Key 2026 (Unofficial)

Here is the Karnataka 2nd PUC Accountancy Answer Key 2026:Question No. | Question | Answer |

|---|---|---|

1 | In order to form a partnership, there should be atleast: | b) Two people |

2 | A, B and C are partners sharing profits in the ratio of 5:3:2. If C retires, the New Profit Sharing Ratio between A and B will be: | b) 5:3 |

3 | Unrecorded liabilities, when paid are shown in: | a) Debit side of Realisation A/c |

4 | Issued capital is a part of: | c) Authorised capital |

5 | Following is an extraordinary item: | d) Loss due to theft |

6 | Partnership comes into existence as a result of ______ among the partners. | Agreement |

7 | Old Ratio - New Ratio = ______ Ratio. | Sacrificing |

8 | On dissolution of a firm, Partner's Loan Account is transferred to ______ Account. | Cash/Bank |

9 | Loans which are repayable within ______ months, are called as short-term borrowings. | Twelve |

10 | Common Size Statement is also known as ______ analysis. | Vertical |

11 (a) | Valuation of goodwill | iv) Average profit method |

11 (b) | Debentures | i) Acknowledgement of debt |

11 (c) | Revenue from operations | v) Sales |

11 (d) | Profitability Ratio | ii) Earnings per share |

11 (e) | Cash flow statement | iii) Inflows and Outflows of cash |

12 | Profit or loss on revaluation is transferred to all partners' capital accounts in case of retirement of a partner. [State True/False] | TRUE |

13 | State any one type of shares. | Equity share (or Preference share) |

14 | What do you mean by Redemption of debentures? | Repayment of the amount of debentures to the debenture holders. |

15 | State any one user of Financial Statement Analysis. | Shareholders (or Investors/Top Management) |

16 | Expand R.O.I. | Return on Investment |

Karnataka 2nd PUC Accountancy Exam 2026: Quick Highlights

Some of the major highlights of the Karnataka 2nd PUC Accountancy exam 2026 have been highlighted here in the following table:

Particulars | Details |

|---|---|

Karnataka 2nd PUC Accountancy exam date | March 14, 2026 |

Exam time | 10 AM to 1 PM |

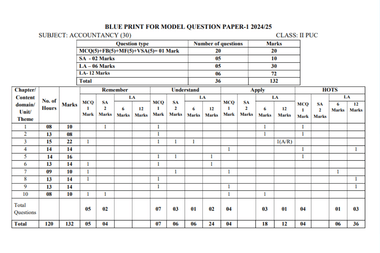

Type of the questions |

|

Mark's distribution for each question |

|

Total number of questions asked | 36 |

Specific instructions for Part A |

|

Specific instructions for Part B |

|

Specific instructions for Part C |

|

Specific instructions for Part D |

|

Also read | Karnataka 2nd PUC Result 2026 Release Date Prediction

Karnataka 2nd PUC Accountancy Exam 2026 LIVE

01 50 PM IST - 14 Mar'26

Karnataka 2nd PUC Accountancy Answer Key 2026 Released!

The Karnataka 2nd PUC Accountancy Answer Key 2026 is out! Students can verify the correct answers with their responses to get an idea about their predicted marks.

01 30 PM IST - 14 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: Exam Ends

Karnataka 2nd PUC Accountancy Exam 2026 ends. Soon, the exam analysis and unofficial answer key will be added here. So that the test takers can assess their performance level.

12 00 PM IST - 14 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: Result Date

KSEAB will likely release the Karnataka 2nd PUC result 2026 tentatively after 4 to 6 weeks from the last date of examination.

11 00 AM IST - 14 Mar'26

Karnataka 2nd PUC Accountancy 2026: One Hour Passed

Two hours to go to complete the Karnataka 2nd PUC Accountancy 2026 exam. Once the exam ends, the unofficial answer keys of the short-type questions and the students' feedback will be added here.

10 00 AM IST - 14 Mar'26

Karnataka 2nd PUC Accountancy 2026: Exam Starts in 15 Minutes

Karnataka 2nd PUC Accountancy Exam 2026 will start in 15 minutes. The candidates will get the question paper at 10.15 AM. Candidates will get 15 minutes to read the question paper.

09 00 AM IST - 14 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: Reporting Starts

The reporting process for the Karnataka 2nd PUC Accountancy Exam 2026 has started. The exam will commence soon.

08 00 AM IST - 14 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: Reporting Will Start Soon

The reporting process for the Karnataka 2nd PUC Accountancy Exam 2026 will begin in one hour, that is at 9 AM. Post that the gate will be closed for reporting at 9.45 AM. No one will be allowed to enter the exam centre once the gate is closed.

07 00 AM IST - 14 Mar'26

12-Marks Heavy Weightage Practice Questions (1/2)

Question: Dissolution of a Firm

X, Y, and Z were partners. They decided to dissolve the firm. Assets realized were: Stock ₹15,000; Machinery ₹25,000; Debtors ₹18,000. Creditors of ₹20,000 were paid at a 10% discount. Realisation expenses amounted to ₹1,000.

Prepare: Realisation Account, Partners' Capital Accounts, and Bank Account.

06 00 AM IST - 14 Mar'26

12-Marks Heavy Weightage Practice Questions (1/1)

Question: Admission of a Partner (The "Must-Know")

P and Q share profits in a 3:2 ratio. Their Balance Sheet shows: Creditors ₹20,000; General Reserve ₹10,000; Capitals: P-₹50,000, Q-₹40,000. Assets: Cash ₹10,000; Debtors ₹30,000; Stock ₹40,000; Building ₹40,000.

R is admitted for a 1/5th share on these terms:

R brings ₹30,000 as capital and ₹10,000 for goodwill.

The building is appreciated by 20%.

The stock has depreciated by ₹5,000.

Provision for Doubtful Debts (PDD) to be created at 5% on Debtors.

Prepare: Revaluation A/c, Partners' Capital A/cs, and New Balance Sheet.

05 00 AM IST - 14 Mar'26

6-Marks Practice Questions (1/2)

Issue of Debentures

$XYZ$ Ltd. issued 2,000, 12% Debentures of ₹100 each. Pass journal entries if:

Debentures are issued at a discount of 5% and are redeemable at par.

Debentures are issued at par and redeemable at a premium of 10%.

04 00 AM IST - 14 Mar'26

6-Marks Practice Questions (1/1)

Question: P&L Appropriation Account

A and B are partners with capitals of ₹1,00,000 and ₹80,000, respectively. Their partnership deed provides for:

Interest on Capital at 10% p.a.

Salary to B at ₹1,000 per month.

Commission to A at ₹5,000 per year.

Interest on Drawings: A - ₹1,200; B - ₹800. Net Profit for the year was ₹60,000. Prepare the P&L Appropriation Account.

03 00 AM IST - 14 Mar'26

Final Exam-Ready Summary

Section A & B: Theory (Partnership Deed, AS-26, Ratio formulas).

Section C (6 Marks): P&L Appropriation, Gaining Ratio, Issue of Debentures.

Section D (12 Marks): Admission/Retirement of a Partner, Dissolution, Issue of Shares.

02 00 AM IST - 14 Mar'26

Differences Between Cash Flow and Fund Flow

Basis of difference Cash Flow Statement Fund Flow Statement Accounting Basis Prepared based on the cash basis of accounting Prepared on an accrual basis of accounting. Time Period Useful for Short-term financial planning and liquidity Useful for Long-term financial planning and solvency. Major Components Divided into Operating, Investing, and Financing activities. Divided into Sources and Applications of Funds. 01 00 AM IST - 14 Mar'26

Objectives of Cash Flow Statement

- To Identify Sources and Applications

- To Assess Liquidity and Solvency

- To Evaluate Financial Flexibility

- To Aid in Short-term Planning

- To Highlight the Difference Between Profit and Cash

12 00 AM IST - 14 Mar'26

Quick Note on Common-Size Statement

For Balance Sheet: Base is Total Assets/Liabilities.

For Income Statement: Base is Revenue from Operations.

11 00 PM IST - 13 Mar'26

Forfeiture of Shares (The "Double Entry" Check)

If a share is forfeited:

- Share Capital A/c is debited with the Called-up amount

- Share Forfeiture A/c is credited with the Amount already received (excluding premium if already paid).

10 00 PM IST - 13 Mar'26

The "Goodwill" Rule (Admission vs. Retirement)

Admission (Sacrifice Ratio): If a new partner brings goodwill, then it is credited to old partners in their Sacrifice Ratio.

- Entry: Cash A/c Dr to Premium for Goodwill -----> Premium for Goodwill Dr to Old Partners' Capital A/c

Retirement (Gain Ratio): When a partner leaves, the continuing partners can then "buy" the share.

- Entry: Continuing Partners' Capital A/c (Gain Ratio) Dr. to Retiring Partner’s Capital A/c

09 40 PM IST - 13 Mar'26

Final Words for Last Night Before Exam

- Do not start any new chapters. Revise those topics that you have already read.

- Try to solve a full-length mock paper before the exam day and self-assess your performance level

- Stay calm and do not panic unnecessarily

09 20 PM IST - 13 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: Realisation "Magic"

Transaction Debit Side of Realisation Credit Side of Realisation Transferring Assets Yes (All except Cash/Bank) No Transferring Liabilities No Yes (Third party only) Payment of Expenses Yes (To bank) No Sale of Assets No Yes (By Bank) Partner taking Liability Yes No 09 00 PM IST - 13 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: The "Unrecorded" Items

Sometimes an asset or liability cannot be seen in the Balance Sheet, but nonetheless appears in the adjustments.

- Unrecorded Asset sold/taken over

- Unrecorded Liability paid

08 40 PM IST - 13 Mar'26

Pro-Tip for 2nd PUC P&L Appropriation Accounts

- Credit Side: Net Profit (from P&L), Interest on Drawings.

Debit side: Interest on Capital, Partner Salary, Partner Commission.

Final Step: Distribute the remaining profit in the given ratio.

08 20 PM IST - 13 Mar'26

Most Repeated 1-Mark Questions

Fill in the blank: The agreement between partners is called __________.

True or False: Interest on Drawings is an income to the partnership firm.

Multiple Choice: Sacrifice Ratio is used to distribute _________ at the time of admission.

(a) Reserves (b) Profits (c) Goodwill (d) Assets

One Word: What is the minimum number of members required to form a Public Company?

Formula: Give the formula for the Quick Ratio.

08 00 PM IST - 13 Mar'26

List of Practice Questions for 5-Marks (1/4)

Topic Name Practice Questions Cash Flow Statement Classify various activities into Operating, Investing, and Financing, such as:

Sale of Machinery

Issue of Debentures

Cash received from Debtors

Purchase of Investments

Interest paid on Bank Loan

07 40 PM IST - 13 Mar'26

List of Practice Questions for 5-Marks (1/3)

Topic Name Practice Questions Company Accounts: Issue of Shares Write the Journal Entries for the Forfeiture and Reissue of shares. Analysis of Financial Statements Prepare a Comparative or Common-Size Income Statement format. 07 20 PM IST - 13 Mar'26

List of Practice Questions for 5-Marks (1/2)

Topic Name Practice Questions Partnership: Admission/Retirement/Death Prepare a Partners' Capital Account of two partners (A and B) with at least 5 imaginary transactions under the Fluctuating Capital System. Partnership: Dissolution Prepare a Realisation Account with 4 imaginary assets (transferred) and 2 imaginary liabilities (paid). 07 00 PM IST - 13 Mar'26

List of Practice Questions for 5-Marks (1/1)

Ques. In a Partners' Capital Account under the Fixed Capital System, where is the 'Interest on Drawings' recorded?

Answer. Debit side of the Current Account.

Ques. In a Common-Size Balance Sheet, what is taken as 100% for calculating the percentage of all other items?

Answer. Total Assets

06 40 PM IST - 13 Mar'26

List of Practice Questions for 12-Marks (1/4)

Ques. On the death of a partner, interest on their capital is calculated from the date of the last Balance Sheet until:

Answer. The date of their death

Ques. A firm has a stock of ₹30,000. In Dissolution, it is realized at 80% of its book value. What is the amount recorded in the Bank Account (Debit side)?

Answer. ₹24,000.

Ques. If the New Partner's Capital is used as the base to adjust Old Partners' Capitals, and the total capital of the firm is ₹1,20,000 with a 3:2:1 ratio, what is the new capital of the first partner?

Answer. ₹60,000.

06 20 PM IST - 13 Mar'26

List of Practice Questions for 12-Marks (1/3)

Ques. X, Y, and Z are partners sharing in 2:2:1. Y retires. The new ratio between X and Z is 3:2. What is the Gaining Ratio?

Answer. 1:1

Ques. A company forfeited 100 shares of ₹10 each (fully called up) for non-payment of allotment money of ₹3 per share. What amount should be credited to the 'Share Forfeiture Account'?

Answer. ₹700

Ques. When shares are reissued at a discount, the amount of discount is debited to which account?

Answer. Share Forfeiture Account

06 00 PM IST - 13 Mar'26

List of Practice Questions for 12-Marks (1/2)

Ques. In a Dissolution problem, the firm has Creditors of ₹20,000. The adjustment states 'Creditors were paid at a discount of 5%'. What amount is debited to the Realisation Account?

Answer. ₹19000

Ques. At the time of Dissolution, if a partner takes over an unrecorded asset of ₹2,000, where is it recorded in the Realisation Account?

Answer. Credit Side05 40 PM IST - 13 Mar'26

List of Practice Questions for 12-Marks (1/1)

Question. A and B are partners (3:2). C is admitted for a 1/6th share. C brings ₹40,000 as capital and ₹12,000 as premium for goodwill. If the Machinery (Book Value ₹50,000) is to be appreciated by 10%, what is the credit entry in the Revaluation Account?

Answer. ₹5000

Ques. In an Admission problem, if the Balance Sheet shows a General Reserve of ₹10,000 and the ratio of old partners A and B is 3:2, how much is credited to A's Capital Account?

Answer. ₹600005 20 PM IST - 13 Mar'26

The "Neatness" Protocol

- Label the working notes clearly. Evaluators give partial marks for working notes, even if the final balance is incorrect.

- It is mandatory to add a heading for every account.

- Don't forget to use the ₹ symbol in your column headers.

05 00 PM IST - 13 Mar'26

Final Accountancy Exam Checklist

- A long ruler (approximately 30 CM)

- Two dark pencils

- Eraser and sharpener

- Black and blue ballpoint pens

- A basic non-programmable calculator

- Karnataka 2nd PUC hall ticket 2026

04 40 PM IST - 13 Mar'26

Pro Tips for 12-Mark Questions on Cash Flow Statement

If the candidates find a surplus (balance in the statement of P&L), then check out the difference between the current and previous years and add back any of the following:

Transfer to General Reserve

Proposed Dividend (Previous Year)

Provision for Tax (Current Year)

04 20 PM IST - 13 Mar'26

The "Cheat Sheet" Tally

Activities Major Focus Key "Add/ Less" Rule Operating Net Profit & Working Capital Add: Depreciation / Less: Tax Paid Investing Fixed Assets & Investments Add: Sale of Asset / Less: Purchase of Asset Financing Share Capital & Loans Add: Issue of Shares / Less: Interest Paid 04 00 PM IST - 13 Mar'26

Financing Activities: Watch the Dividends

Particulars Details Inflow Issue of Shares, Issue of Debentures, and Taking a Bank Loan Outflow Redemption of Debentures, Payment of Interest, Payment of Dividend The Dividend Rule Use the Proposed Dividend of the Previous Year for payment in the current year's CFS 03 45 PM IST - 13 Mar'26

Investing Activities: The Ledger Trick

If the candidates will get "Opening Balance, "Closing Balance," and "Depreciation" for an asset like Machinery, then they should draw a quick T-account in the rough sheet.

Debit side: Opening Balance + Purchases (Balancing Figure).

Credit side: Depreciation + Sale Value + Closing Balance.

03 30 PM IST - 13 Mar'26

Operating Activities: The "Inverse" Rule of Cash Flow Statement

Non-Cash/Non-Operating Items Working Capital Changes Depreciation.

Loss on Sale of Fixed Assets.

Interest Paid.

- Increase in Current Assets

- Decrease in Current Assets

- Increase in Current Liabilities = Add & Decrease in current liabilities = Subtract

03 15 PM IST - 13 Mar'26

The Three-Story Building of Cash Flow Statement

The Cash Flow Statement is categorised into three sections:

- Operating Activities that is the main business

- Investing Activities, that is, the "Assets"

- Financing Activities, that is, the "Capital/ Debt"

03 00 PM IST - 13 Mar'26

How to Approach the Exam (3-Hour Plan)

- First 15 minutes: Question reading time. During this time, the candidates should identify the best 3 (out of 6) questions of 12 marks

- In the next 90 minutes, the candidates should complete all the 12-mark and 6-mark problems.

- In the next 60 minutes, candidates should finish 1 mark MCQs, 2 marks short answer type questions

- In the last 30 minutes, the candidates should tally the balance sheets, check the Journal Narrations, and make sure that the question numbers match the answer sheet.

02 45 PM IST - 13 Mar'26

Practice Questions for The "Raised and Written Off"

P and Q are partners (1:1). They admit R. Goodwill of the firm is valued at ₹30,000. R is unable to bring his share of goodwill in cash. Partners decide to raise and write off the goodwill. The new profit-sharing ratio is 2:2:1.

Task: Pass the two necessary journal entries.

02 30 PM IST - 13 Mar'26

Practice Questions for Retirement

A, B, and C are partners sharing profits in the ratio of 5:3:2. B retires from the firm. The goodwill of the entire firm is valued at ₹50,000. A and C decide to share future profits in the ratio of 3:2.

Task: Calculate B’s share of goodwill and pass the adjustment entry.

02 15 PM IST - 13 Mar'26

Practice Questions for Treatment of Goodwill

X and Y are partners sharing profits in the ratio of 3:2. They admit Z into the partnership for a 1/5th share. Z brings ₹20,000 as his capital and ₹10,000 as his share of the premium for goodwill.

Task: Pass the journal entries for the treatment of goodwill.

02 00 PM IST - 13 Mar'26

Quick Revision Guide: Cash Flow Classification

Particulars Details Operating Anything related to day-to-day business (such as the sale of goods, Payment to creditors, Salaries, Income Tax). Investing Related to Fixed Assets and Investments (e.g., Purchase of Machinery, Sale of Land, Interest/Dividend received). Financing Related to Capital and Loans (e.g., Issue of Shares, Redemption of Debentures, Interest paid on Loans, Dividends paid). 01 30 PM IST - 13 Mar'26

Final Exam "Do's and Don'ts"

- Draw paper formats for journal and ledger accounts using a scale and pencil. It is accounted as "Presentation of Marks".

- Do not forget "Narration" in journal entries. (For eg, the short explanation starts with "being)

- Do attempt Practical Oriented Questions at the end (5 marks each). They are very simple, such as "Prepare a specimen of a Share Certificate" or "Classify Assets and Liabilities."

01 15 PM IST - 13 Mar'26

Top Repeated 2-Mark Questions from Financial Analysis

Mention any two objectives of Financial Statements.

State two examples of "Cash Equivalents."

Define Cash Flow Statement.

01 00 PM IST - 13 Mar'26

Top Repeated 2-Mark Questions from Company Accounts

Define a Company or a Prospectus.

State any two types of Share Capital (e.g., Authorized, Issued, Subscribed).

What is "Minimum Subscription"?

12 45 PM IST - 13 Mar'26

Top Repeated 2-Mark Questions from Dissolution

What is a Realisation Account?

Give the journal entry for an asset taken over by a partner.

12 30 PM IST - 13 Mar'26

Top Repeated 2-Mark Questions from Reconstitution (Admission/Retirement)

What is Sacrifice Ratio? (Used during Admission).

What is Gain Ratio? (Used during Retirement).

Mention any two circumstances for the retirement of a partner.

12 15 PM IST - 13 Mar'26

Top Repeated 2-Mark Questions from Partnership Basics (Section B)

Define Partnership (as per Section 4 of the Indian Partnership Act, 1932).

What is a Partnership Deed?

State any two features of partnership (e.g., Two or more persons, Agreement, Profit sharing).

State any two differences between the Fixed Capital Method and the Fluctuating Capital Method.

12 00 PM IST - 13 Mar'26

Top 10 Most Frequent Theory Questions (1/4)

Topic Question Capital Reserve Where is the profit on the reissue of forfeited shares transferred? Financial Statement Analysis Name any two tools of financial analysis. 11 40 AM IST - 13 Mar'26

Top 10 Most Frequent Theory Questions (1/3)

Topic Question Equity Shares vs. Preference Shares What is the prime difference between Equity and Preference shares? Meaning of "Over-subscription" What is over-subscription of shares? 11 20 AM IST - 13 Mar'26

Final Game Plan for Saturday Morning

- 7 AM to 7.30 AM: Quickly revise the ratio Analysis formulas, such as Current, Liquid, Debt-Equity.

- 7.30 AM to 8.00 AM: Revise the short notes on Journal Ethics

- 8.30 AM to 9 AM: Look at the cash flow statement

11 00 AM IST - 13 Mar'26

Top 10 Most Frequent Theory Questions (1/2)

Topic Question Answer Sacrifice Ratio vs. Gaining Ratio Why is the Sacrifice Ratio calculated? It is calculated at the time of Admission in order to distribute the share of goodwill of the new partner among the old partners Why is the Gaining Ratio calculated? It is calculated during the time of Retirement/Death, so that the amount the remaining partners should pay for the outgoing partner's share of Goodwill can be determined. Accounting Standard 26 How should Goodwill be treated as per AS-26? Goodwill should be recorded in the books only when the consideration in money has been paid for it. 10 45 AM IST - 13 Mar'26

Top 10 Most Frequent Theory Questions (1/1)

Topic Question Answer Partnership Deed What is a Partnership Deed? It is nothing but the written agreement between the partners containing the terms and conditions of the partnership. Fluctuating vs. Fixed Capital State one difference between Fixed and Fluctuating Capital Accounts. In Fixed Capital, two accounts are maintained (both Capital and Current). On the other hand, in Fluctuating Capital, only one account (Capital) is maintained for all transactions. 10 30 AM IST - 13 Mar'26

The Final Check Logic: Dissolution of Partnership Firm

If Credit > Debit: Realisation Profit (Transfer to Partners' Capital A/c).

If Debit > Credit: Realisation Loss (Transfer to Partners' Capital A/c).

10 15 AM IST - 13 Mar'26

Common "Karnataka Board" Pitfalls related to Dissolution of Partnership Firm

- Do not transfer the partner's loan to the Realisation Account. It is paid separately after outside liabilities but before partners' capital.

- If a partner was supposed to pay realisation expenses but the firm paid on their behalf, debit the Partner's Capital A/c.

- In Dissolution, treat Goodwill like any other asset, such as Furniture. Transfer it to the debit side. If it's sold, credit the amount received.

10 00 AM IST - 13 Mar'26

Pro Tips for 12-Mark Problem Asked From Dissolution of Partnership Firm (1/3)

Partner takes Asset: Record on the Credit side

Partner pays Liability: Record on the Debit side

09 45 AM IST - 13 Mar'26

Pro Tips for 12-Mark Problem Asked From Dissolution of Partnership Firm (1/2)

Treatment of Provisions (PDD):

Transfer the Gross Debtors (full amount) to the Debit side.

Transfer the Provision (PDD) to the Credit side of the Realisation Account.

Note that the PDD is never "paid"; it just adds on the credit side for balancing the book value of debtors.

09 30 AM IST - 13 Mar'26

Pro Tips for 12-Mark Problem Asked From Dissolution of Partnership Firm (1/1)

The "Silent" Liability Rule:

- If an asset's realized value is not given, then assume it realized Zero (don't record anything on the credit side).

- If a liability's payment value is not given, then one should pay it off at 100% book value on the debit side.

09 15 AM IST - 13 Mar'26

Short Notes on The Realisation Account Flow

- Step 1: Transfer all the assets to the debit side at their Book value (Balance Sheet Value).

- Step 2: Transfer the outside liabilities to the Credit side.

- Step 3: Record the cash received from the sale of assets on the credit side.

- Step 4: Record the payments made on the debit side.

09 00 AM IST - 13 Mar'26

Inverse Rule for Current Assets

Increase in Current Assets = Subtract from Operating Profit.

Decrease in Current Assets = Add to Operating Profit.

(Current Liabilities follow the normal rule: Increase = Add, Decrease = Subtract).

08 45 AM IST - 13 Mar'26

Important Formulas on Common-Size & Comparative Statements

- Comparative Statement % Change: [Absolute Change (Current Year- Previous Year)]/ Previous Year Value X 100

- Common Size Statement %:

- Balance Sheet = Individual Item/(Total Assets/ Liabilities) X 100

- Income Statement = (Individual Item/ Revenue from Operations) X 100

08 30 AM IST - 13 Mar'26

Important Formulas on Company Accounts (Shares & Debentures)

Amount Transfer to Capital Reserve = (Amount Forfeited/ Number of Shares Forfeited) X Number of Shares Reissued.

08 15 AM IST - 13 Mar'26

Important Formulas on Analysis of Financial Statements (1/2)

Ratio Formula Gross Profit Ratio (Gross Profit/ Net Revenue from Operations)X100 Inventory Turnover Cost of Revenue from Operations/ Average Inventory 08 00 AM IST - 13 Mar'26

Important Formulas on Analysis of Financial Statements (1/1)

Ratio Formula Ideal Ratio Current Ratio (Current Assets/ Current Liabilities) 2:1 Quick (Liquid) Ratio [Quick Assets (Current Assets- Stock- Prepayments)]/ Current Liabilities 1:1 Debt-Equity Ratio Long-term debts/Shareholders' Funds 2:1 07 45 AM IST - 13 Mar'26

Important Formulas on Decreased Partner's Share of Profit (Death)

Profit = Previous Year's Profit X (Months Lived/ 12) X Decreased Partner's Share

07 30 AM IST - 13 Mar'26

Important Formulas on Interest on Drawings (Average Period Method)

- Beginning of each month: Interest = Total Drawings X Rate X (6.5/12)

- Middle of each month: Interest = Total Drawings X Rate X (6/12)

- End of each month: Interest = Total Drawings X Rate X (5.5/12)

07 15 AM IST - 13 Mar'26

Important Formulas on Partnership Accounts

- Sacrificing Ratio (Admission): Used to distribute Goodwill, that is, Old Ratio- New Ratio.

- Gaining Ratio (Retirement/Death): Used to compensate the outgoing partner; that is, New Ratio- Old Ratio.

- New Profit Sharing Ratio (NPSR), that is, Old share- Sacrifice.

07 00 AM IST - 13 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: 1-Mark MCQs Sample Questions (1/3)

Ques. At the time of dissolution, 'Realisation Account' is a:

Answer. National Account

Ques. In a Realisation Account, if an unrecorded liability is paid, it is recorded on the:

Answer. Debit Side

Ques. The Gaining Ratio is calculated as:

Answer. New Ratio- Old Ratio

Ques. If assets are transferred to the Realisation Account at ₹50,000 but are realized only at ₹40,000, the difference of ₹10,000 is a:

Answer. Realisation Loss

06 45 AM IST - 13 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: 1-Mark MCQs Sample Questions (1/2)

Ques. According to Accounting Standard 26 (AS-26), Goodwill can only be recorded in the books of accounts when:

Answer. Money or money's worth has been paid for it.

Ques. Profit or Loss on Revaluation at the time of admission is shared by:

Answer. Old partners in the old ratio.

Ques. On the death of a partner, the amount due to them is transferred to:

Answer. Their Executor's Account.

06 30 AM IST - 13 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: 1-Mark MCQs Sample Questions (1/1)

Ques. In the absence of a Partnership Deed, what is the rate of interest allowed on a partner's loan to the firm?

Answer. 6% per annum

Ques. If a partner draws ₹2,000 at the beginning of every month and interest is charged at 10% p.a., for how many months should the average interest be calculated?

Answer. 6.5 months.

Ques. The ratio in which old partners agree to forego their share of profit in favor of a new partner is called:

Answer. Sacrificing Ratio

06 15 AM IST - 13 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: Presentation Strategy

- KSEAB evaluators will give additional marks for working on notes (such as the calculation of a new ratio or goodwill distribution); hence, do not skip them.

- Use a scale for drawing lines. Neatness in the Realisation A/c and Revaluation A/c can prevent calculation errors.

- In a 12-Mark question, if the candidates do not tally the Balance sheet, then do not panic and scratch everything out.

06 00 AM IST - 13 Mar'26

Quick Score-Boosters from Partnerships: 6-Marks Questions

- P&L Appropriation: Always check the "Interest on Drawings". If the date is not given, then calculate it for 6-months. (This is an average period)

- Guarantee of Profit: If a partner is guaranteed a minimum amount, then the deficiency will be borne by the other partners in their specific ratio.

05 45 AM IST - 13 Mar'26

The "Golden Trio" of Partnership Chapters

- Retirement & Death of a Partner

- Dissolution of a Firm

- Admission of a Partner

05 15 AM IST - 13 Mar'26

Common Pitfalls to Avoid

- If the provision increases, then the increased amount will be added to the Revaluation Debit Side.

- Only distribute the "excess" amount to the partners after keeping aside what is required for a claim.

- Make sure that the new partner's Capital and their share of goodwill are added to the Cash/Bank balance in the new Balance Sheet.

05 00 AM IST - 13 Mar'26

Karnataka 2nd PUC Accountancy Exam 2026: Last Minute Preparation Tips

- Focus on Partnership: since candidates will receive 16 marks from each Chapter 3 and 4, their primary focus should be on Revaluation Accounts and Realisation Accounts.

- Format Matters, and for the same, the candidates should create the Balance sheets and Ledger accounts properly. It is better to use a ruler for neat columns.

- Practice the entries for Share Capital since these are the most weighted calculation-based sections.

- Solve model papers as much as possible to familiarize yourself with the blueprint.